This indicator measures the harvest levels of wood products in relation to future yields. The capacity to implement strategies to deal with changing demand for forest products based on future yields from both native and plantation forests is an integral part of sustainable forest management.

This part of Indicator 2.1c: Annual removal of wood products compared to the volume determined to be sustainable for native forests, and future yields for plantations, published October 2024, presents forecast sustainable yields and log supply from native forests and commercial plantations.

- The forecast supply of high-quality logs from public multiple-use native forests will continue to decrease following the ending of commercial wood harvesting in some states in 2024 and from the impact of the 2019-20 bushfires on growing stock.

- The annual plantation log availability is forecast to gradually increase to the year 2060, albeit more slowly than previously forecasted following impacts from the 2019-20 bushfires and a decrease in the area of hardwood plantations.

- Total plantation softwood log availability (most of which is sawlogs) is forecast to increase from 15.3 million cubic metres per year in the period 2020-24 to 19.2 million cubic metres per year in the period 2050-54. Sawn timber from softwood plantations is typically used for housing and general construction.

- Total plantation hardwood log availability (most of which is pulplogs) is forecast to range between 9.5 and 11 million cubic metres per year for the entire 2020-64 forecast period. Hardwood plantations are typically managed for the production of pulplogs for use in the production of paper and paperboard.

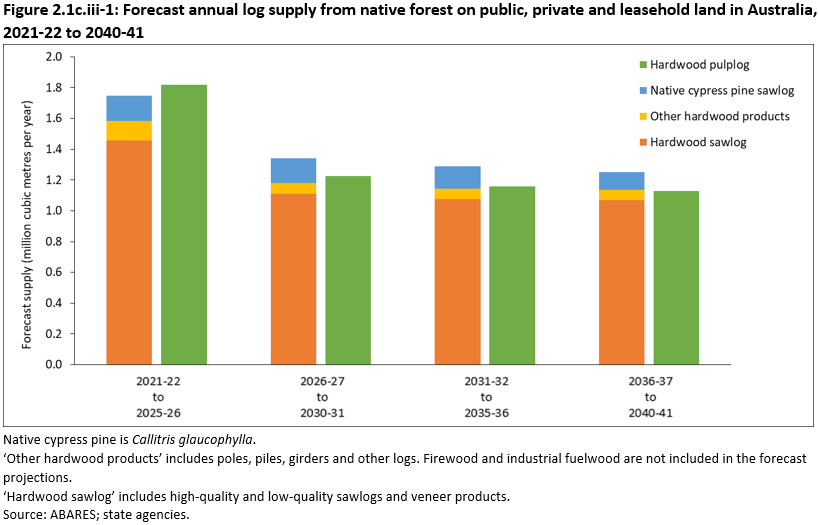

The forecast annual native forest hardwood sawlog supply is 1.5 million cubic metres from 2021-22 to 2025-26 and then dropping to 1.1 million cubic metres from 2026-27 (Figure 2.1c.iii-1). Supply of pulplogs is forecast at 1.8 million cubic metres per year from 2021-22 to 2025-26 and then dropping to 1.2 million cubic metres per year in the following period (Figure 2.1c.iii-1). This compares with the average of 1.7 million cubic metres of native forest hardwood sawlogs and 1.9 million cubic metres of native forest pulplogs harvested per year between 2016-17 and 2020-21 (Indicator 2.1c.ii, Figures 2.1c.ii-5 and 2.1c.ii-4).

The forecast decrease of supply reflects the ending of commercial wood harvesting in multiple-use public native forests in some states, and the impact of the 2019 20 bushfires on growing stock. The forecast combines both the decrease in sustainable yield of native forest sawlogs from multiple-use public forests over the forecast period and an anticipated increase in supply from private native forests as processors who have traditionally sourced wood from public native forests seek raw materials from other sources. The trend of an increase in sawlog supply from private native forests during the reporting period 2016-17 to 2020-21 is expected to continue. The forecast supply from private native forests is based on likely proportional increases to historical harvest levels, however, the actual supply from private native forests will depend on market forces, the objectives and goals of private forest owners, and the relevant native forestry regulatory framework at the time.

Click here for a Microsoft Excel workbook of the data for Figure 2.1c.iii-1.

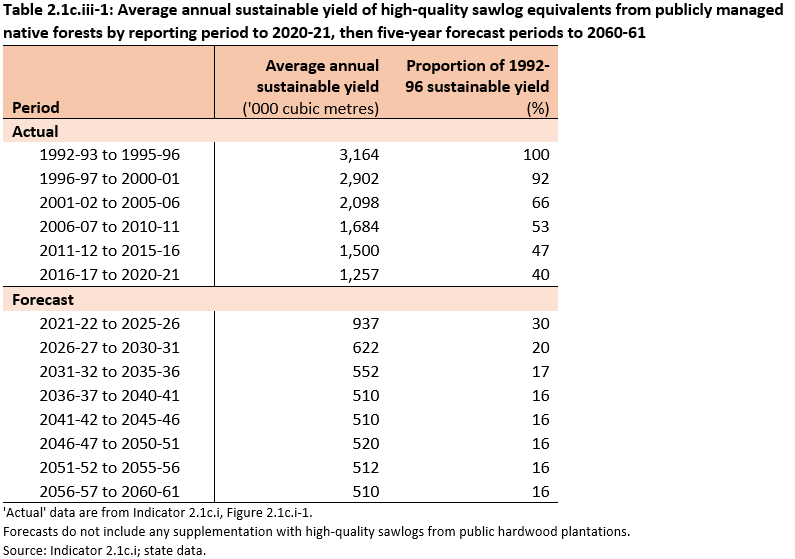

The average annual sustainable yield of high-quality sawlogs from publicly managed native forests in the 2016-17 to 2020-21 reporting period (1,257 thousand cubic metres) was reduced to 40% of the sustainable yield in the 1992-93 to 1995-96 reporting period (3,164 thousand cubic metres). A further reduction to 16% of the estimated sustainable yield in the first period is forecast from 2036-37 (510 thousand cubic metres) onwards (Table 2.1c.iii-1). These forecasts are supplied by the five states that have traditionally harvested high-quality sawlogs from public native forest: New South Wales, Queensland, Tasmania, Victoria and Western Australia.

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-1.

The sustainable yield forecasts for publicly managed forests presented in Table 2.1c.iii-1 factor in:

- Victorian Government policy to end commercial wood harvesting in public native forests in Victoria from 01 January 2024

- Western Australian Government policy to end large-scale commercial wood harvesting in public native forests in Western Australia from 01 January 2024

- Queensland Government policy regarding the ending of commercial wood harvesting in public native forests within the South East Queensland Regional Plan area from 01 January 2025

- the transition of high-quality hardwood sawlog supply from predominately native forests to predominately hardwood plantations in Tasmania from 2028 onwards, and the associated reduction in forecasted native forest volumes

- the impact of the 2019-20 bushfires on growing stock and sustainable yields in New South Wales (FCNSW 2020).

The Western Australian Forest Management Plan 2024-2033 (CPC 2023) provides for limited ongoing supply of logs sourced from clearing of public native forests for mining or infrastructure, and ecological thinning operations. However, there is uncertainty at this stage about the likely volume by log grade and species mix that may arise, and this source has not been included in the forecasts.

These forecasts assume that there are no further reductions, or additions to net harvestable area, beyond those listed above. Sustainable yield forecasts are subject to change and are regularly reviewed at the state level to incorporate further changes in reservation, code prescriptions, disturbance and climate change.

The forecasts also assume the ongoing satisfactory management of risk from bushfire, disease and climate impacts. However, the frequency of high-intensity, large-scale bushfires is predicted to increase in Australia with climate change (Abram et al. 2021). Depending on species, mature trees have varying responses after bushfire. Some species recover well after being impacted by bushfire (such as spotted gum, Corymbia maculata, and ironbark spp.), while others are killed outright by even moderate intensity fires (such as alpine ash, Eucalyptus delegatensis). Generally, high-intensity fire will compromise young regrowth stems and cause a level of defect in future log products. Therefore, increasing frequency of high-intensity fires may further reduce sustainable yields. There is also evidence that increasing temperature may reduce the growth rates of some important commercial Australian hardwood species (Bowman et al. 2014; Wardlaw 2024).

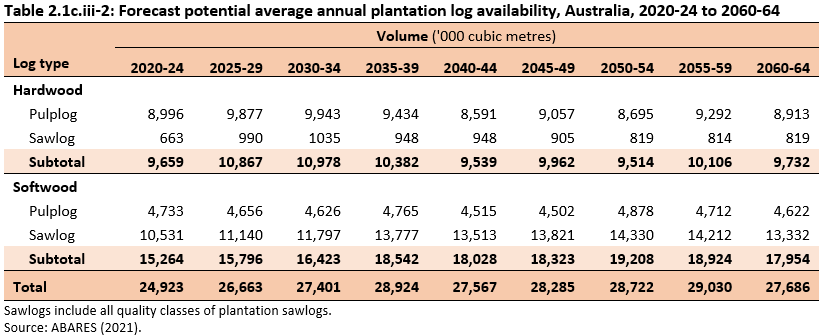

The potential average annual plantation log availability is forecast to increase from 24.9 million cubic metres in the 2020-24 period to 29.0 million cubic metres by the 2055-59 period (Table 2.1c.iii-2). There has been a decrease in the log availability estimates across the early forecast periods from previous ABARES (2016) estimates due to tree mortality after the 2019-20 ‘Black Summer’ bushfires and a decrease in the hardwood plantation estate area.

Plantation softwood log availability is forecast to gradually increase from 15.3 million cubic metres per year in the 2020-24 period to a peak of 19.2 million cubic metres per year in the 2050-54 period (Table 2.1c.iii-2). The peak is primarily associated with softwood plantations replanted after the 2019-20 bushfire season reaching maturity.

Most of the sawn timber used for housing and general construction in Australia is sourced from plantation softwood sawlogs. The availability of plantation softwood sawlogs is forecast to increase from 10.5 million cubic metres per year in the 2020-24 period to 14.3 million cubic metres per year in the 2050-54 period (Table 2.1c.iii-2).

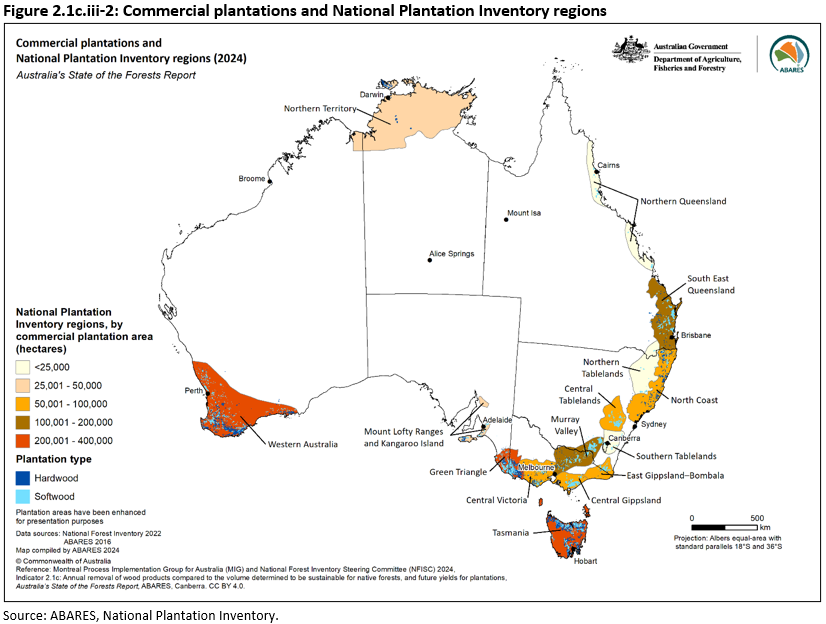

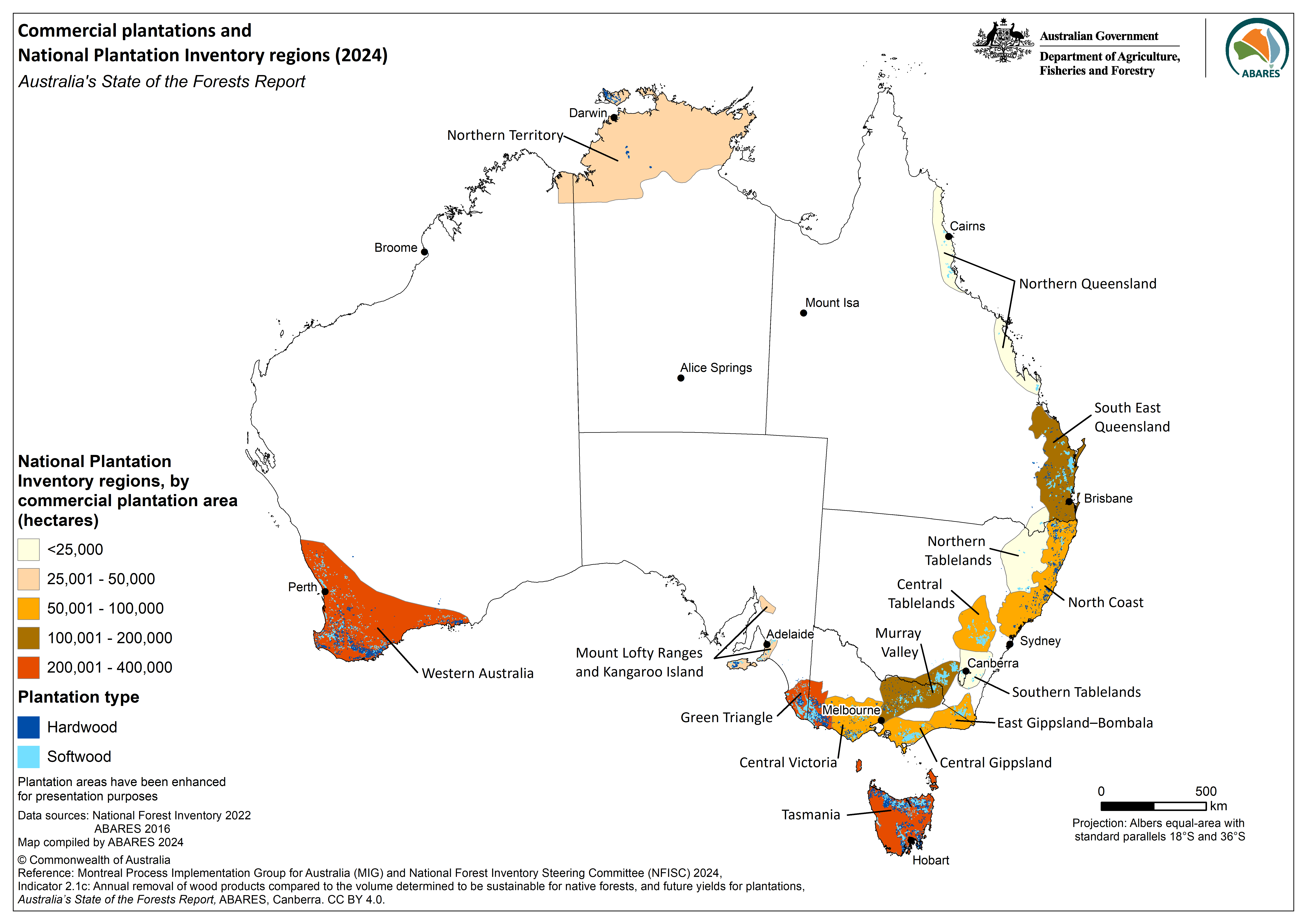

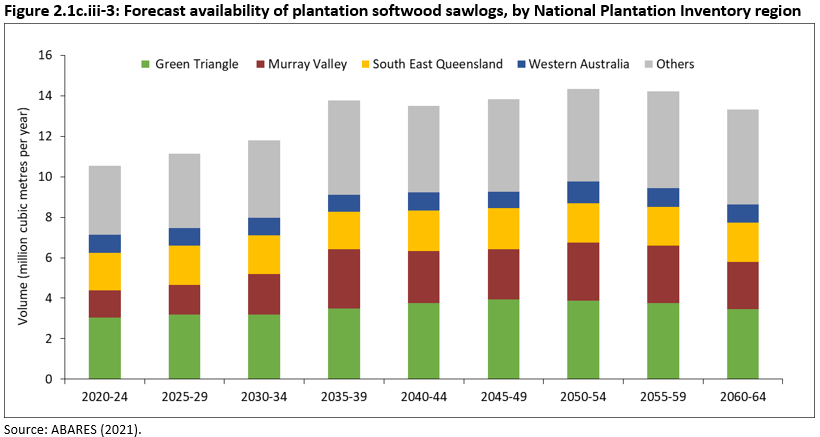

Australia’s commercial plantations are primarily based in 15 National Plantation Inventory (NPI) regions (Figure 2.1c.iii-2). The Western Australia, Green Triangle and Tasmania NPI regions each contain estates of more than 200 thousand hectares of commercial plantations. The Green Triangle, Murray Valley and South East Queensland NPI regions are forecast to produce the majority of the plantation softwood sawlogs available over the entire forecast period 2020-2064, contributing an average of 27%, 18% and 15% of the total national available softwood sawlog volume respectively (Figure 2.1c.iii 3).

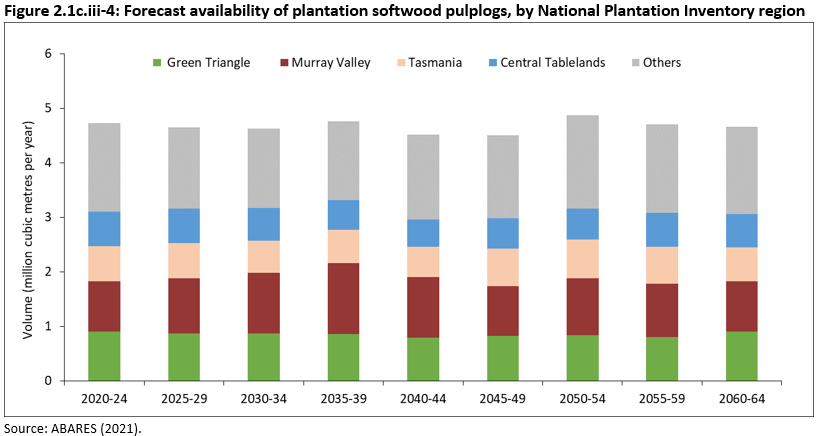

Plantation softwood pulplog availability is forecast to vary around an average annual volume of 4.7 million cubic metres throughout the forecast period (Table 2.1c.iii-2). The Murray Valley, Green Triangle and Tasmania NPI regions are forecast to be the main softwood pulpwood producing regions, contributing an average of 22%, 18% and 14% of the total national available pulplog volume, respectively (Figure 2.1c.iii-4).

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-2.

Click here for high-definition copy of Figure 2.1c.iii-2.

{kind=link}

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-3.

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-4.

Total plantation hardwood log availability is forecast to hover between 9.5 million cubic metres and 11.0 million cubic metres per year for the entire 2020-64 forecast period (Table 2.1c.iii-2). Hardwood plantations in Australia are primarily managed for growing pulplogs for use in the production of paper and other related products.

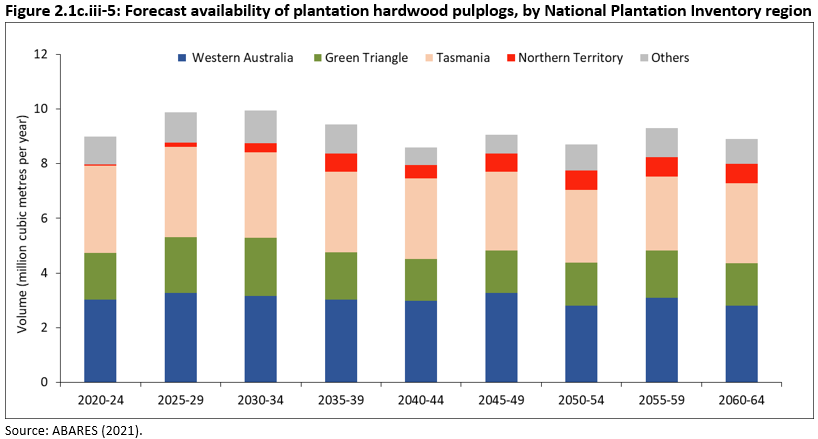

Plantation hardwood pulplog availability is forecast to vary around an annual average of 9.2 million hectares for the 2020-64 forecast period (Table 2.1c.iii-2). The Tasmania, Western Australia and Green Triangle NPI regions are forecast to be the main hardwood pulplog producing regions accounting for 32%, 33% and 19% of the national total respectively (Figure 2.1c.iii-5). The Northern Territory NPI region is also forecast to supply significant volumes of hardwood pulplogs from 2035-39 as higher yielding plantations are established in the second rotation (ABARES 2021).

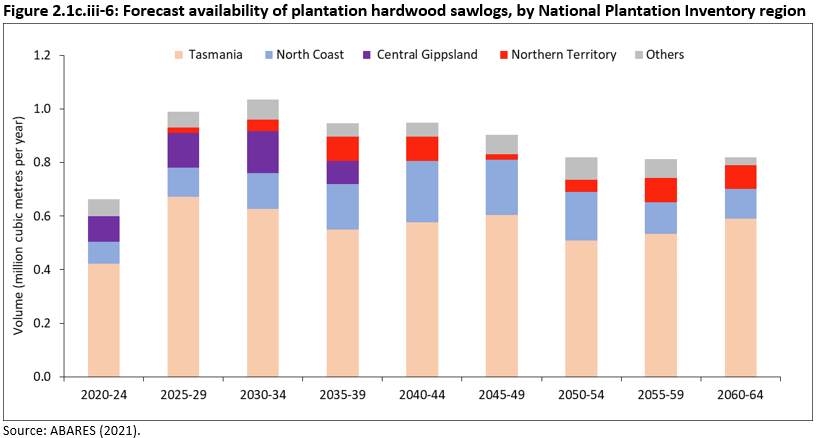

To date, increases in area of hardwood plantations have not resulted in substantial increases in harvested sawlog volume. However, plantation hardwood sawlog availability is expected to increase from an annual average of 0.66 million cubic metres in 2020-24 to 1.0 million cubic metres in 2030-34 (36% increase). From 2035-39, the average annual plantation hardwood sawlog yield is forecast to vary around an annual average of 0.88 million cubic metres (Table 2.1c.iii-2 and Figure 2.1c.iii-6). Tasmania and North Coast NPI regions are forecast to be the main sources of plantation hardwood sawlogs throughout the entire 2020-64 forecast period, with 64% and 17% of national total availability respectively. The Central Gippsland NPI region is forecast to supply significant volumes during 2020-39, and modest volumes are forecast to become available from the Northern Territory NPI region from the 2025-29 period (Figure 2.1c.iii-6).

The forecast potential future log availability from existing plantations to 2060-64 (Table 2.1c.iii-2) assume that most harvested areas will be replanted with the same plantation species after harvesting (ABARES 2021). For each type of plantation, log availability forecasts consider the area of existing plantations by year of establishment and the assumed rotation length, silvicultural regimes (including thinning), and growth rates. However, commercial plantation estates are managed as businesses, so the timing and volume of log harvests is determined mainly by market forces, rotation length and thinning regimes. Thus, market supply and demand will influence the actual volumes that are harvested at any given time and plantation replanting.

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-5.

Click here for a Microsoft Excel workbook of the data for Table 2.1c.iii-6.

ABARES (Australian Bureau of Agricultural and Resource Economics) (2016). Australia’s plantation log supply 2015-2059, Australian Bureau of Agricultural and Resource Economics, Canberra. CC BY 3.0.

ABARES (Australian Bureau of Agricultural and Resource Economics) (2021). Australian plantation statistics and log availability report 2021, Australian Bureau of Agricultural and Resource Economics, Canberra. CC BY 4.0. doi.org/10.25814/xj7c-p829

Abram J, Henley B, Sen Gupta A, Lippmann T, Clarke H, Dowdy A, Sharples J, Nola R, Zhang T, Wooster M, Wurtzel J, Meissner K, Pitman A, Ukkola A, Murphy B, Tapper N and Boer M. (2021). Connections of climate change and variability to large and extreme forest fires in southeast Australia, Communications Earth and Environment 2,8. doi.org/10.1038/s43247-020-00065-8

Bowman D, Williamson G, Keenan R and Prior L (2014). A warmer world will reduce tree growth in evergreen broadleaf forests: evidence from Australian temperate and subtropical eucalypt forests, Global Ecology and Biogeography 23:925-934. doi.org/10.1111/geb.12171

CPC (Conservation and Parks Commission) (2023). Forest Management Plan 2024–2033, Conservation and Parks Commission, Perth.

FCNSW (Forestry Corporation of NSW) (2020). 2019-20 Wildfires: NSW Coastal Hardwood Forests Sustainable Yield Review, Forestry Corporation of NSW, Sydney.

Wardlaw T (2024). Giants Under Threat: The vulnerability of Tasmania’s tall eucalypt forests to a warming climate. Terrestrial Ecosystem Research Network, The University of Queensland, Brisbane.