Authors: Tim Goesch, Peter Legg and Manannan Donoghoe

Summary

The Murray-Darling Basin (MDB) water market is complex and influenced by a range of factors, including weather, commodity markets and water policy. The objective of this report is to shed some light on changes in water markets (water prices and water trade flows) in the MDB over the past 15 to 20 years, and to explain the main factors driving these changes.

A key feature of the MDB water market is that the total volume of water available for use is capped, with changes in the supply and demand for water reflected in the price of water and movements in water between farms, industries and regions.

Historical data shows that water allocation prices are mainly driven by changes in water supply (Figure 1), and that the main factor influencing water supply in the MDB is rainfall. Rainfall was around 17 per cent lower than the long run average in the southern MDB (sMDB) during the Millennium drought, and has been 5 per cent lower since 2000. This has led to significantly lower inflows into rivers and dams. Allocation prices increased to unprecedented highs during the peak of the Millennium drought before declining to near zero following the 2011, 2012 and 2016 floods. Prices have risen substantially again during the latest drought.

Source: Price data is sourced from the BOM national water register, various market reports and broker websites; ABS Consumer Price Index (2019) (cat. 6401.0). Storage data is from Water NSW, SA Water, Goulburn-Murray Water, and the MDBA.

Other factors influencing supply

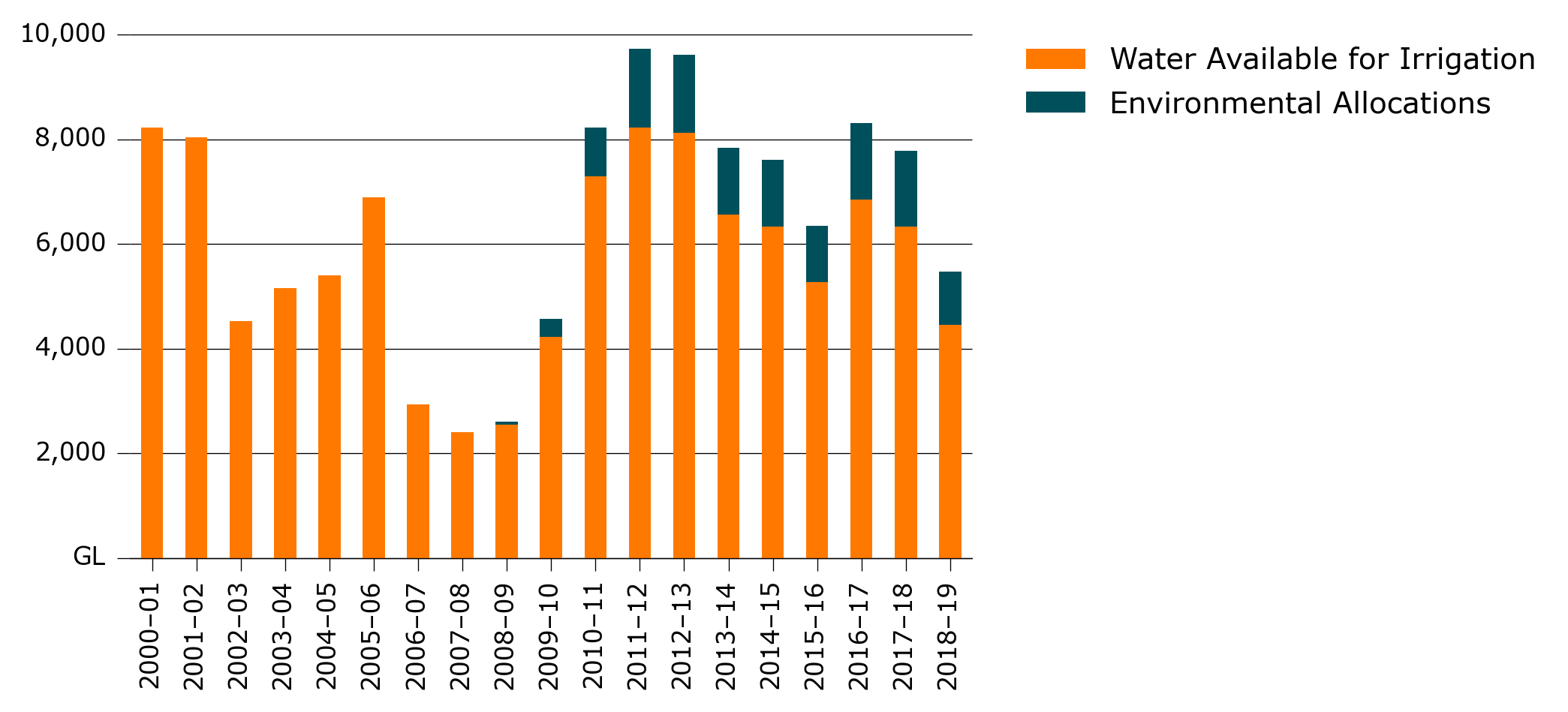

The other factors influencing supply tend to be institutional, and include recovering water for the environment, restrictions on interregional trade, changes in allocation rules in state water sharing plans and increased access to carryover. Commonwealth environmental recovery contributes to higher prices by reducing the volume of water available for irrigation (Figure 2) while trade restrictions can lead to differences in prices between regions in connected systems. Changes in the way water is allocated in state water sharing plans can change the timing of supply. For example, new water storage policies and more conservative forecasts for future inflows can change the timing of allocations, both within and between years.

Source: ABARES estimate

There has been significant interest in the impact that Commonwealth environmental water recovery has had on water supply and water prices in recent years. While Commonwealth environmental water recovery has reduced consumptive supply, the effect has been relatively small compared to the effect rainfall had on supply over the same period.

The effect of increasing access to carryover on supply is more complex. Carryover allows irrigators to have more control over the timing of water use. The easing of restrictions on carryover that occurred in the late 2000s contributed to a significant increase in carryover balances during the high rainfall years that followed the Millennium drought. This was followed by a period of drawdown as rainfall declined. The increased use of carryover has important implications for the allocation market. In general, carryover will lead to slightly higher prices in years when carryover reserves are being accumulated (typically average or wetter years), and lower prices in years when carryover reserves are drawn down (typically drier years). It also has implications for where water is used and what it is used for. For example, in the absence of carryover, most of the water accumulated in carryover accounts in wetter years would have been used for lower value activities or sold on the allocation market.

Changes in demand since early 2000s

There have also been significant changes in the demand for irrigation water in the MDB since the early 2000s. This is particularly the case in the sMDB where genetic advances and movements in commodity prices have led to an increase in the demand for water for cotton and almonds and a decrease in demand for rice, dairy pastures and grapevines (Figure 3). ABARES modelling suggests that this change in the composition of demand away from some of the more flexible lower value activities such as pastures and rice to higher value annual activities such as cotton and perennial activities such as almonds means that the demand for water will be higher at most water prices. The exception is when prices are very low, in which case demand is estimated to be similar.

This shift in demand has led to changes in the location of water use and interregional trade flows in the sMDB. For example, the increase in demand for water for almonds has occurred mainly in the Victorian Murray below the Barmah choke, with this expansion facilitated by interregional trade, mainly from regions above the Barmah choke. Increased demand below the Barmah choke and tighter restrictions on interregional trade have resulted in trade limits binding more often in the sMDB. This was particularly the case in 2016–17, when these limits restricted trade into the downstream Murray trading zones, contributing to higher allocation prices in these zones, and lower allocation prices in the upstream trading zones (including in the Murrumbidgee, Goulburn and above Barmah choke trading zones). Research by Aither (2019) suggests that the demand for water for permanent plantings in the sMDB could increase from current levels as existing plantings mature. This could lead to an increase in the frequency restrictions on interregional trade are binding.

Gupta & Hughes (2018) modelled future water prices in the sMDB assuming 2016-17 levels of water demand, 2016-17 institutional arrangements and a repeat of the historical climate between 2002-03 and 2016-17. The estimates suggest that there could be a change in the distribution of future allocation prices in the sMDB, with fewer years with low prices and more years with moderate to high prices.

Download the full report

Murray-Darling Basin water markets: trends and drivers 2002-03 to 2018-19 PDF [3.9 MB]

Murray-Darling Basin water markets: trends and drivers 2002-03 to 2018-19 DOCX [17.8 MB]