Opportunities for Australian agricultural producers

Authors: Jared Greenville, Heather McGilvray, and Kevin Burns

Introduction

The challenge of reducing greenhouse gas emissions is a global one. As countries plan to meet this challenge, the emissions intensity of products will increasingly become part of global trading rules. This creates opportunities for Australia’s agricultural exports.

Climate change is impacting the productivity and profitability of Australian farmers. The sector is already adapting, and will benefit from global action to limit the extent of further change. The Paris Agreement provides a framework for that global action to occur, but its implementation will be driven by bottom-up decisions—by individual countries setting emission reduction targets and policies, and by consumers, businesses and industries as they position themselves on the issue of reducing emissions. As an exporting sector, Australian agriculture has an interest in how country-level policies develop, and in the effectiveness of global action. The sector can gain by leading discussion on emissions and trade, and by establishing itself as a high value, lower emissions intensity producer.

[expand all]

Global action to limit climate change is particularly important for agriculture

Australia has a naturally variable climate, but around that variability, the climate is changing. Average temperatures in Australia have increased by about 1.4°C since 1910, mostly since 1950.

The frequency of extreme heat events and droughts has increased and there has been a shift towards drier conditions across southwestern and south-eastern Australia during April to October (BoM & CSIRO 2020) (Figure 1).

ABARES analysis shows that conditions over the last 20 years have negatively affected the profits of both cropping and livestock farms, relative to conditions experienced from 1950 to 2019 (Figure 2; Hughes et al. 2019). The effects were most pronounced in the cropping sector, amounting to an average loss in production of around $1.1 billion per year, with the frequency of negative profit years increasing to one in four years, rather than one in ten years.

While there is uncertainty about the nature and pace of future climate change in Australia, the changes are unlikely to provide net benefits to agriculture.

Source: ABARES farmpredict in Hughes et al. 2019

Global ambition is expected to increase, towards ‘net zero’ emissions

The Paris Agreement provides a framework for all countries to tackle the challenge of climate change. It aims to limit the increase in the average global temperature to well below 2°C, and ideally to 1.5°C, to avoid more significant climate change risks.

To achieve that goal, global emissions need to peak as soon as possible and then fall to ‘net zero’ globally in the second half of the century (UNFCCC 2015; IPCC 2018). At ‘net zero’, emissions would be balanced by carbon sinks.

The Agreement establishes that common goal. But each country is responsible for determining its targets and policies. Under the Agreement, national commitments are to be formalised, regularly reviewed, and made progressively more ambitious.

Recent analysis finds that aggregate commitments currently fall short of what is needed to reach the Paris goals. Without more ambition, the result is expected to be around 3.2°C of global warming, rather 1.5 or 2°C (UNEP 2019).

Given the economic benefits of limiting warming (see, for example, Stern 2008; Heal 2009; Nordhaus 2010; Kompas et al. 2019), pressure for more ambition is expected to build internationally. The next formal round of international discussions will be held on 1-12 November, 2021. In the lead up, countries are continuing to develop their longer term plans.

A growing number are setting net zero targets (Figure 3). Some jurisdictions have already legislated or proposed legislation for these commitments, including the EU, the UK and New Zealand. Importantly, three of Australia’s largest trading partners, China, Japan and Korea, have recently announced carbon neutral goals. And for several countries, the transition to lower emissions is forming part of their plans for economic recovery after COVID-19.

Net zero goals are also being set by sub-national governments, including all Australian states and territories, as well as by individual companies.

Source: Based on Energy & Climate Intelligence Unit 2020 .

As economies transition, new rules and preferences will emerge

As economies transition towards lower emissions, opportunities may emerge for sectors that can demonstrate more emissions-efficient production systems, or even carbon neutrality. Conversely, slower-moving sectors may become exposed and less competitive under changing regulatory and market structures.

These opportunities are likely to exist for sectors within countries with low emission targets, but also for those that trade into those economies.

For example, the EU has already said it expects free trade agreement partners to respect and implement Paris Agreement targets. The EU and UK are also considering the use of carbon border adjustments to ensure that actions taken in their economies are not offset by the effect of imported products (CCC 2019; Von de Leyen 2019).

If countries implement such measures, their domestic emission standards would effectively be imposed on exporting countries, like Australia. For agriculture, emissions intensity would become another factor influencing the sector’s export competitiveness.

Emissions intensity may also influence competitiveness at the more micro level; with some consumers and food companies.

Recent high profile studies have brought the emissions from food production to the attention of consumers.

The 2019 EAT-Lancet report has set out diets that could help constrain emissions growth and warming. In this report, the authors argue that substantial reductions in the production and consumption of red meat could both reduce emissions and improve human health (Willet et al. 2019).

It is yet to be seen whether a significant number of consumers will respond by adjusting their purchasing decisions. But consumers increasingly want food that is high quality, safe and sustainable. There may be first mover advantages for producers who are ready to respond to concerns about emissions as part of an overall strategy for improving competitiveness.

Parts of Australian agriculture are already responding. The Australian red meat industry has a goal to be carbon neutral by 2030. The industry is establishing pathways to the target, including use of existing and prospective livestock and land management practices (Mayberry et al. 2018). It is also reporting regularly on emissions as part of an overall sustainability framework. GrainGrowers supports a net zero goal for agriculture by 2050 and is aiming to release a grain-specific target for 2030. Other sectors are also acting, and the sector’s national body, the National Farmers’ Federation, has endorsed a goal for the Australian economy to reach net zero emissions by 2050.

Individual businesses are also responding. For example the Northern Australian Pastoral Company (NAPCo) has obtained a carbon neutral product certification under the Australian Government’s ‘Climate Active’ scheme.

Land use emissions have declined; but agricultural emissions remain static

Agricultural emissions are currently 75.6Mt (CO2-e), contributing around 14% of Australia’s national emissions (2018). Around 77% of that is methane; produced by livestock during digestion and in manure management. The remainder is nitrous oxide from crop residue burning and fertiliser use (19% of agricultural emissions), and carbon dioxide from lime and urea application (4% of agricultural emissions).

The sector also contributes to national emission outcomes via its land use decisions—including management of vegetation and soils. These emissions are generally not classified as agricultural emissions in national and international greenhouse gas reporting frameworks under the UNFCCC; but agriculture, forestry and land use (AFOLU) are often grouped together in discussions about the emissions impact of the sector.

Agricultural emissions have been relatively static over the last 30 years; shifting up or down with changes in the livestock sector and farms transitioning between different production systems (Figure 4 and Figure 5). In contrast, land use emissions have declined significantly (Figure 4). Much of that was a result of reduced land clearing.

Source: National Greenhouse Gas Inventory – UNFCCC classifications (DISER 2020)

Source: National Greenhouse Gas Inventory – UNFCCC classifications (DISER 2020)

Emissions intensity of production may form part of competitiveness

While historical changes are important to recognise, it is likely that as countries transition to more ambitious targets, the focus will be on the emissions impact of current production. Producers are unlikely to be credited with past performance. And as an exporting sector, Australian agriculture can expect to have its performance compared with producers in importing countries and with export competitors.

Global comparisons are complex, and should be based on validated data and sound and widely accepted methods (including the definition and ‘boundary’ of production for emissions accounting purposes). However, current global data and assessments suggest Australia should be well placed to compete on this basis.

Analysis by Poore and Nemecek (2018) suggests a potential natural advantage for Australian producers, with wheat and grass-fed beef farms below the global median in terms of emissions intensity. FAO data on emissions also suggests that Australian beef producers are more efficient (in emissions per unit of production) than many of the world’s large exporting nations with whom we compete in world markets (Figure 6).

Note: *Country or region is both a major importer and a major exporter. The chart shows FAO estimates of the emissions intensity of top ten exporters and importers of beef in terms of volume. Dashed lines are weighted average across those exporters and importers. Rest of world not presented on left hand chart due to significant variation across the grouping.

However, Australia’s emissions intensity is higher than domestic industry levels in many of the world’s major beef importing nations. These countries may seek to leverage their lower emissions intensity via trade rules.

The EU’s stated intention to impose a carbon border tax to ensure that EU companies can compete on a level playing field is relevant in this context.

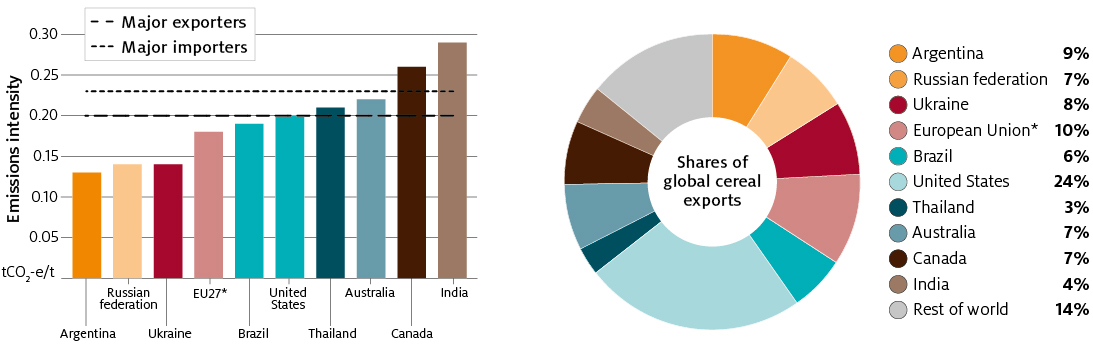

For cereals, Australia is above the weighted average for exporting nations, and below the weighted average for importing nations (Figure 7).

Note: *Country or region is both a major importer and a major exporter. The chart shows FAO estimates of the emissions intensity of top ten exporters and importers of cereals in terms of volume. Dashed lines are weighted average across those exporters and importers. Rest of world not presented on left hand chart due to significant variation across the grouping.

Given uncertainties about data, these global comparisons are only illustrative. But the message for Australian producers is that improvements in emissions intensity could increase the sector’s competitiveness in some markets. The challenge for industry and governments is to ensure that Australian producers have access to technologies and practices that enable them to continually improve their emissions performance at the lowest cost possible to remain competitive.

Innovation and investment need to decouple emissions from production

It is not practical to think that all emissions will be eliminated from agriculture given the natural system within which the sector operates. Emission reduction policies should aim to incentivise the most economically efficient options available across the economy, and many of these would not be in agriculture in the first instance.

However there are a range of existing options available to Australian farmers which would improve emissions intensity and productivity. They include reducing or changing farm input use, capturing emissions (most relevant to intensive production) or changing herd management to increase growth rates. Uptake may be an issue, influenced by farm type, size and region, as well as economic, personal, social and cultural factors (Kuehne et al. 2011; Mallawaarachchi et al. 2009).

But looking to the future, there is a need for cost-effective options which more significantly decouple emissions from production, particularly for livestock. Earlier research has identified possible areas for further work, including feed supplements, genetics, vaccination and early life programming of livestock. Some of these are more prospective than others, but those with the highest mitigation and productivity potential also generally require the highest investment (Meat & Livestock Australia 2015).

Source: Shutterstock.com

A proactive approach to market rules and certification will benefit the sector

The challenge of reducing emissions in agriculture is a global one.

For exporters like Australia, policy in trading partners and influential markets may prove significant. There are likely to be opportunities for those that can demonstrate more emissions-efficient production. Australian producers appear relatively well placed to compete on this basis. The challenge is to ensure that trade arrangements and certification systems are evidence-based and suit Australian production systems. A proactive approach by industry and government will help ensure this occurs.

There are options for Australian producers to differentiate their product in markets based on emissions intensity of production. Examples include the Australian Government’s Climate Active (formerly National Carbon Offset Standard). However, given agriculture’s export reliance, a more systematic approach to market access and global trading rules would be in agriculture’s interest, particularly for the meat and livestock sectors.

Improving emissions intensity will be an important part of the competitiveness strategy of Australian agriculture. In the longer term, cost effective new options and innovations will be needed which allow emissions and production to be more substantially decoupled.

Source: Shutterstock.com

References

BoM & CSIRO 2020, State of the Climate 2020, Bureau of Meteorology and Commonwealth Scientific & Industrial Research Organisation.

Committee on Climate Change (CCC) 2019, Net Zero - Technical Report, United Kingdom, London, May.

Department of Industry, Science, Energy and Resources (DISER) 2020, National Greenhouse Gas Inventory

– UNFCCC classifications, Australian Greenhouse Emissions Information System (AGEIS).

Energy & Climate Intelligence Unit 2020, Net Zero Tracker, https://eciu.net/netzerotracker/map.

Food and Agriculture Organization of the United Nations (FAO) 2020, FAOSTAT: Food and agriculture data, Rome, accessed 17 July, 2020.

Heal, G 2009, Climate economics: A meta-review and some suggestions for future research, Review of Environmental Economics and Policy, Oxford University Press for Association of Environmental and Resource Economists, vol. 3(1), pages 4-21, Winter (pdf 225kb).

Hughes, N, Galeano, D, Hatfield-Dodds, S 2019, The effects of drought and climate variability on Australian farms, Australian Bureau of Agricultural and Resource Economics and Sciences, Canberra.

Intergovernmental Panel on Climate Change (IPCC) (2018), Summary for Policymakers. In: Global Warming of 1.5°C. An IPCC Special Report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty [Masson-Delmotte, V., P. Zhai, H.-O. Pörtner, D. Roberts, J. Skea, P.R. Shukla, A. Pirani, W. Moufouma-Okia, C. Péan, R. Pidcock, S. Connors, J.B.R. Matthews, Y. Chen, X. Zhou, M.I. Gomis, E. Lonnoy, T. Maycock, M. Tignor, and T. Waterfield (eds.)]. World Meteorological Organization, Geneva, Switzerland, 32 pp.

Kompas, T, Pham, VH, Tuong, NC 2019, The effects of climate change on GDP by country and the global economic gains from complying with the Paris Accord, Earth's Future, August, vol. 6, issue 8, pp. 1153–1173.

Kuehne, G, Llewellyn, R, Pannell, D, Wilkinson, R & Dolling, P 2011, ADOPT: a tool for predicting adoption of agricultural innovations (pdf 186kb).

Mallawaarachchi, T, Walcott, J, Hughes, N, Gooday, P, Georgeson, L & Foster, A 2009, Promoting productivity in the agriculture and food sector value chain: issues for R&D investment (pdf 600kb), ABARE and BRS report to the Rural R&D Council, Canberra, December.

Mayberry, D, Bartlett, H, Moss, J, Wiedemann, S, Herrero, M 2018, Greenhouse gas mitigation potential of the Australian red meat production and processing sectors, Meat & Livestock Australia Limited, North Sydney.

Meat & Livestock Australia (MLA) 2015, More meat, milk and wool: Less methane.

Nordhaus, W 2010, Economic aspects of global warming in a post-Copenhagen environment, PNAS, June 29, 2010 107 (26) 11721-11726.

Organisation for Economic Co-operation and Development (OECD) 2015, The Economic Consequences of Climate Change, OECD Publishing, Paris.

Poore, J & Nemecek, T 2018, Reducing food’s environmental impacts through producers and consumers, Science 01 Jun 2018: vol. 360, issue 6392, pp. 987–99.

Stern, N 2008, The economics of climate change, American Economic Review, Papers & Proceedings 2008, 98:2, 1-37.

United Nations Environment Programme (UNEP) 2019, Emissions Gap Report 2019, UNEP, Nairobi.

United Nations Framework Convention on Climate Change (UNFCCC) 2015, Paris Agreement.

Von de Leyen 2019, Mission Letter to Commissioner-designate for Trade.

Willett, W, Rockström, J, Loken, B, Springmann, M, Lang, T, Vermeulen, S, Garnett, T, Tilman, D, DeClerck, F, Wood, A, Jonell, M, Clark, M, Gordon, LJ, Fanzo, J, Hawkes, C, Zurayk, R, Rivera, JA, De Vries, W, Majele Sibanda, L, Afshin, A, Chaudhary, A, Herrero, M, Agustina, R, Branca, F, Lartey, A, Fan, S, Crona, B, Fox, E, Bignet, V, Troell, M, Lindahl, T, Singh, S, Cornell, SE, Srinath Reddy, K, Narain, S, Nishtar, S and Murray, CJL 2019, Food in the Anthropocene: the EAT-Lancet Commission on healthy diets from sustainable food systems, The Lancet, 393 (10170), pp. 447–492.

Download the report